As Western lenders retreat, African banks see an opportunity

Their pan-continental plans have not paid off Yet

ADE AYEYEMI’S office in Lomé, the capital of Togo, is a good place to think about crossing borders. Ghana is ten minutes’ drive away. From his window the boss of Ecobank can watch trucks rumble along the seafront, some bound for Burkina Faso, a day’s journey, or Mali, perhaps another day on. At night, cargo ships twinkle offshore. From here Ecobank’s vision—“to integrate the continent”, Mr Ayeyemi says—is clear. Whether it will be profitable is less obvious.

ADE AYEYEMI’S office in Lomé, the capital of Togo, is a good place to think about crossing borders. Ghana is ten minutes’ drive away. From his window the boss of Ecobank can watch trucks rumble along the seafront, some bound for Burkina Faso, a day’s journey, or Mali, perhaps another day on. At night, cargo ships twinkle offshore. From here Ecobank’s vision—“to integrate the continent”, Mr Ayeyemi says—is clear. Whether it will be profitable is less obvious.

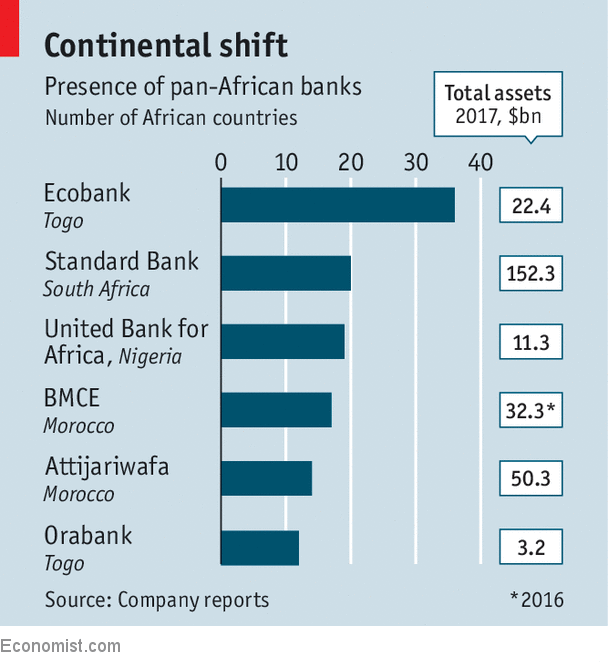

Ecobank was founded in 1985 by business leaders with backing from the Economic Community of West African States, a regional bloc. It has branches in 33 countries, more than any other African bank (see chart). It is not alone in its ambitions. Nigeria’s United Bank for Africa (UBA) wants to make half its profits elsewhere in the continent by 2022. South Africa’s Standard Bank recently opened in Ivory Coast, its 20th African country. Moroccan banks are trekking across the Sahara.

African bankers have long preached some version of what Tony Elumelu, UBA’s chairman, calls “Africapitalism”: the idea that far-sighted, home-grown businesses can drive development. In Nigeria banking reform in 2005 set off a wave of consolidation. The survivors were heftier and more profitable, with capital to invest abroad. Kenyan banks have used their edge in innovation, such as mobile banking, to push into neighbouring markets.

Regional banks are now filling gaps left by their European and American rivals, which are retreating from a continent they once dominated. Barclays sold a majority stake in its African business last year. Other global giants have also reduced their exposure to African markets, which they judge too small and too risky in an era of tightened regulation. African banks work closer to the ground. “Banking is a relationship game,” says Ugochukwu Nwaghodoh, chief financial officer of UBA. “We have local knowledge.”

The pan-African vision often clashes with the reality of a fragmented continent. Africa’s regional banks earn lower returns and grow more slowly than domestic rivals, calculate consultants at McKinsey. One problem is the wide diversity of regulations and markets. Another is that banks are too small outside their core markets to grow organically, says Olamipo Ogunsanya, an analyst at Renaissance Capital. Some have made risky acquisitions, inheriting loan books with hidden troubles. Most banks, she argues, would do better to focus on a few key countries.

Consider Ecobank. The board ousted a previous boss in 2014 over allegations of mismanagement. In 2016 a recession in Nigeria, its biggest market, resulted in a $131m pre-tax loss. It has shut 74 branches there and laid off 2,000 staff. It has scaled back its ambitions beyond west Africa. Although it has returned to profit, about 10% of its loans are non-performing. Expansion may have been too rapid, Mr Ayeyemi admits.

But regional bankers see two big trends in their favour. The first is new technology, says Mr Ayeyemi, which makes it possible to operate on a continental scale as never before. Ecobank can design products and process data centrally, he notes, providing services even where it lacks physical branches. Is Africa’s diversity a problem? “You don’t ask Unilever the same question,” he replies, likening retail banking to selling consumer goods. Ecobank’s mobile app, which lets people open accounts on their phones, has attracted over 5m users since its launch in 2016.

The other helpful trend is the spread of regional banks’ corporate clients. A recent study by the Boston Consulting Group finds that the top 30 African companies now operate in an average of 16 countries, twice as many as a decade ago. Standard Bank’s clients range from construction firms to airlines, says Sola David-Borha, who heads its operations on the continent outside South Africa. “They are helping to grow our market share, as we use our expertise to support their expansion.”

Regional banks are also using their geographical reach to act as natural conduits for cross-border flows of capital, such as migrants’ remittances. Mr Nwaghodoh argues that UBA’s large footprint reduces the cost of intra-African trade, since the bank can stand at both ends of the transaction. He also cites the example of the aid sector, where donors need a “last-mile” presence to distribute cash or pay workers.

The growth of cross-border banking carries risks, says Amadou Sy of the IMF. Regulators need to patch the holes through which a crisis in one country could leak into another. A supervisory college for Ecobank, comprising regulators from the countries where it operates, first met in 2015. European experience shows that such measures are not always enough, warns Thorsten Beck of Cass Business School in London. “When a bank actually fails,” he says, “then the politics comes in.” Although most African banks hold plenty of capital, problem loans have been rising.

Yet Mr Sy also notes that regional banks can spur competition and export innovation. A study by Mr Beck published in 2015 found that African firms got loans more easily when foreign banks held a larger market share—as long as those banks came from Africa or elsewhere in the developing world. Expansion has not yet paid off for Africa’s banks. But, like the incoming waves beyond Mr Ayeyemi’s window, they have the tide behind them.